Mar 3, 2023

What are Scope 3 emissions? And why should you report them?

What are Scope 3 emissions? And why should you report them?

In November 2022, the European Council introduced a new reporting requirement for corporate sustainability. From 2025, companies in Europe, including those based elsewhere with European operations, will be required to report indirect emissions across their value chain; these are known as Scope 3 emissions. But how should companies go about meeting this requirement? Find out below, and see why the increased attention on Scope 3 emissions can help companies identify their greatest emissions-reduction opportunities.

The race to reduce greenhouse gas (GHG) emissions relies heavily on global standards for measurement. This enables companies to compare themselves against one another as well as against global benchmarks. This thinking led to the GHG Protocol being formed in the late 1990s from a partnership between the World Resources Institute and the World Business Council for Sustainable Development. They saw the need for an international standard for GHG accounting and reporting.

In 2001, the GHG Protocol first published its Corporate Standard, and this was revised in 2004. Today, the GHG Protocol is the most common set of standards in GHG accounting. It serves as the main global standard for entities in the public and private sector to measure, report and manage their GHG emissions. It is a standard that encompasses both direct and indirect emissions.

A standard of three scopes

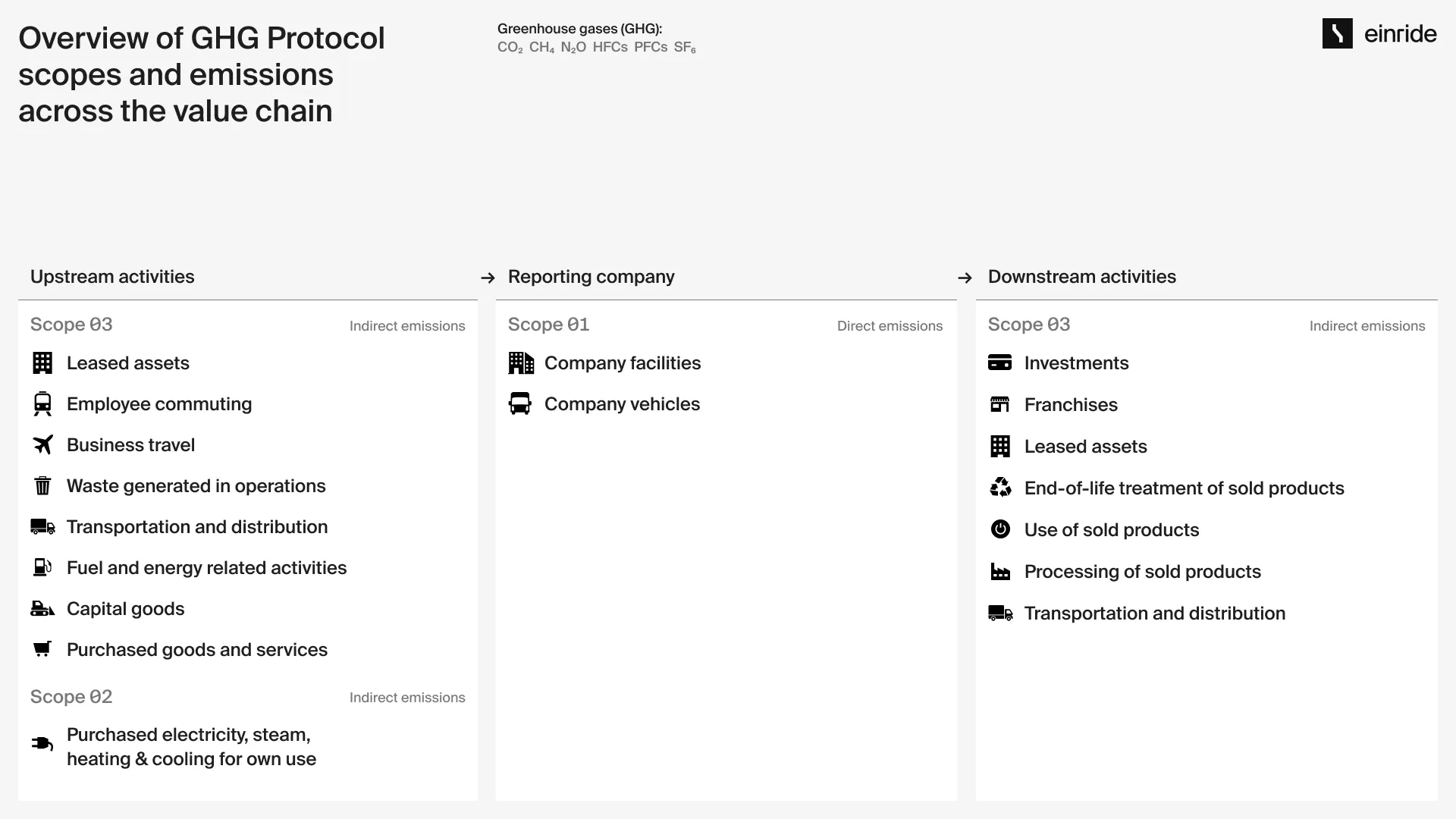

Under the Corporate Standard, a company’s emissions are classified into three scopes.

Scope 1 emissions: These are the emissions from operations that are owned or controlled by the company that’s doing the reporting.

Scope 2 emissions: These are emissions caused by the generation of electricity, steam, heating or cooling that is then consumed by the reporting company.

Scope 3 emissions: These are all indirect emissions (not included in Scope 2) that occur in the value chain of the reporting company, including both upstream and downstream emissions.

The table below shows how the GHG Protocol classes emissions generated across the value chain into one of three reporting scopes.

Up until now, companies have only been required to account for and report all Scope 1 and 2 emissions. However, a company’s most significant emissions often come from the value chain activities – that is, Scope 3 emissions.

This makes for quite a substantial gap in accounting. That’s because in general, a company’s supply chain produces 11 times as much emissions according to PwC as its own operations.

“In general, a company’s supply chain produces 11 times as much emissions as its own operations.”

New reporting standards for Europe from 2025

This “gap” in reporting has prompted regulatory measures to be introduced. In November 2022, the European Council approved the new Corporate Sustainability Reporting Directive (CSRD) which is a combination of all existing reporting standards, including the GHG Protocol.

The implications are clear. By 2025, companies are required to report and publish more detailed information on sustainability matters including all direct and indirect emissions up and down the value chain.

As part of the new EU requirement, companies must report how they will support in reaching the Paris Agreement’s target of limiting global warming to 1.5°C, including the companies’ emission reduction targets and their strategy for how to reach them. The reporting must also be verified by an independent third party.

Who does CSRD apply to?

The CSRD will replace the 2014 non-financial reporting directive (NFRD). It will apply to all large companies as well as all companies listed on regulated markets that currently report according to NFRD, except for listed micro-undertakings.

Despite the new directive being applicable in the EU, the directive impacts non-European companies as well. All non-European companies generating a net turnover of EUR 150 million in the EU, and which have at least one subsidiary or branch in the EU, must provide a sustainability report on their impact.

Why report Scope 3 emissions?

In addition to regulatory compliance, there are several reasons why companies should measure and report their direct and indirect emissions. As Scope 3 emissions often represent the largest source of emissions according to the GHG Protocol, they also present the most significant opportunity to reduce GHG emissions.

Through better visibility across the full value chain, companies can identify emissions hotspots they may have been unaware of. This enables them to target the greatest reduction opportunities and thus proactively, and effectively, work towards a more sustainable supply chain.

Measuring and reporting Scope 3 emissions is an effective way for companies to show stakeholders – including investors, customers and employees – that they understand their impact on the environment, and are working actively to consciously reduce their overall footprint.

“This presents an important opportunity for companies to proactively manage their value chain sustainability.”

“The EU’s new requirement mandating the reporting of Scope 3 emissions will not only increase companies’ awareness of their environmental and societal impact but also empower them to take concrete steps towards emission reduction,” says Mehdi Akbarian, Head of Product Strategy at Einride.

“This presents an important opportunity for companies to proactively manage their value chain sustainability. By actively partnering with suppliers to reduce emissions and improve efficiency throughout the value chain, companies will significantly contribute to a more sustainable future for our planet, reduce their transport costs, and increase productivity of their supply chain.”

The 15 categories of Scope 3 emissions

Scope 3 emissions are the result of activities from assets not owned or controlled by a company, but that the company indirectly affects in its value chain, such as material suppliers, third-party logistics providers, franchisees, etc.

There are 15 categories according to PwC of Scope 3 emissions – eight of them encompass upstream emissions and seven encompass downstream emissions. Upstream emissions are released as a result of the production, processing, and transportation of a product or service. Downstream emissions are released as a result of the consumption of a product or service.

It is important to review both upstream and downstream emissions as they both contribute to the overall GHG footprint of a product or service.

How to report Scope 3 emissions

The Scope 3 Standard provides requirements and guidance for how to report a GHG emissions inventory that includes Scope 3 emissions. Through a standardized step-by-step approach, companies will be able to understand the full impact of GHG emissions:

Define business goals

Review accounting & reporting principles

Identify Scope 3 activities

Set the Scope 3 boundary

Collect data

Allocate emissions

Set a target (optional) & track emissions over time

Assure emissions (optional)

Report emissions

For a full summary of all steps on how to prepare and report GHG emissions, refer to The Scope 3 Standard. According to EU regulations, the report must be presented in the required electronic reporting format and uploaded to the upcoming European Single Access Point (ESAP).

Reporting approaches and the benefits of primary data

Depending on the company’s goals, resources, and data availability, Scope 3 emissions can be calculated and reported using one of three different approaches:

Spend-based: Calculations of Scope 3 emissions are based on the financial value of all purchased goods or services multiplied by an emission factor, which is estimated through secondary data, such as industry-average data, financial data, etc.

Supplier-specific: Calculations of Scope 3 emissions are based on primary operational data directly from the suppliers, multiplied by an emission factor of the operations.

Hybrid: This approach is a combination of the above two, where supplier-specific data is used whenever available, and the remaining is calculated through spend-based.

The supplier-specific approach is the most accurate approach as it provides a more detailed and correct representation of an organization's specific value chain activities. For this approach, complete and accurate primary data is essential to calculate emissions and track performance.

As part of the emissions reporting, companies are required to report the types and sources of data used, as well as the percentage of used primary data. To the greatest extent, companies should collect and report primary data from suppliers and other value chain partners.

With Einride, primary transportation data is only one click away

Upstream and downstream transportation and distribution represent category 4 and category 9 within Scope 3 emissions. For companies that are involved in the production, distribution or use of goods, transportation can represent a major proportion of their overall emissions.

Emissions for upstream and downstream transportation are often calculated through rough estimations because of the large number of actors often involved when it comes to logistics. This makes it difficult for companies to obtain primary-quality data.

For shippers who use Einride as their transportation provider, there is no need to do estimations for calculating transportation emissions. These shipper businesses can easily collect all primary transportation data needed through Einride’s digital freight platform.

The intuitive software also enables these shippers to generate reports and receive actionable sustainability insights, such as which routes to electrify for the greatest impact. It also provides real-time details on shipping KPIs, emissions, energy usage, and performance. Beyond getting a clearer snapshot of their environmental footprint, businesses can discover impactful ways to improve on their operational, financial and environmental KPIs while reducing inefficiencies.

The emissions data provided by Einride has been externally validated. The Global Logistics Emissions Council is a coalition of 150+ organizations working to reduce emissions across global supply chains; its GLEC Framework has been developed to offer multinational businesses and their suppliers a harmonized, efficient, and transparent way to calculate and report logistics emissions. In 2023, Einride’s emission calculation methodology was officially accredited under Smart Freight Centre’s GLEC framework.

Ship with Einride to reduce emissions with ease

Regardless of the share of a company’s total emissions, transportation represents one of the greatest opportunities for most companies to reduce emissions. Einride provides shippers with a “one-stop” solution for electrifying their transportation operations without complexity or costly overhead investments. For companies wanting to make the switch to electric shipping, Einride can provide a tailored, end-to-end assessment showing how to introduce smarter shipping operations in a seamless and cost-efficient way.

Get in touch with us to get an electrification assessment →

Einride

Signup to our newsletter

Signup to our newsletter